Background

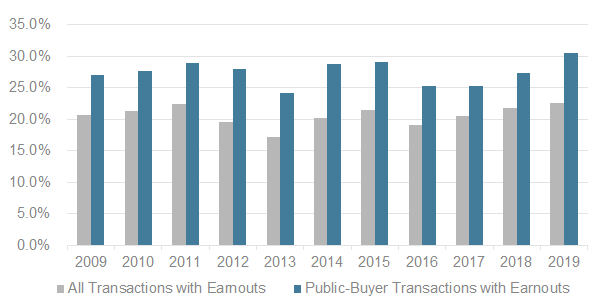

Contingent considerations (or earnouts) are utilized in M&A transactions when companies structure a portion of the purchase consideration to be contingent on the future performance of the acquired business. Contingent considerations remain a popular means to reconcile different expectations regarding the future performance of the acquired business, provide alternative forms of financing, or incentivize an existing management team post acquisition. Over the 2009–2019 period, contingent considerations were present in approximately 25%–30% of public-buyer transactions.

Figure 1: Percentage of Transactions With Contingent Considerations

Source: S&P Capital IQ, internal research

According to Accounting Standard Codification (ASC) Topic 805: Business Combinations, an acquirer is required to report the contingent consideration transferred at fair value as part of the purchase price. Furthermore, as many contingent considerations are classified as liabilities on the balance sheet of the acquiring entity, many acquirers are required to revalue, or “mark-to-market,” contingent considerations at each subsequent reporting period until the final settlement of the obligation.

Valuation Considerations

Contingent considerations often have option-like, leveraged payouts when compared to the underlying performance metrics on which they are based. Furthermore, the introduction of hurdle thresholds and aggregate caps complicates the relationship between the valuation inputs used in modeling the contingent consideration payments and the concluded fair value for the instrument.

Many companies may opt to take a higher level approach on quarterly valuation dates in more stable markets. However, due to the complex option-like payoff of contingent considerations, current market conditions can give rise to both nonintuitive and large value changes. The table below highlights typical inputs in the valuation of contingent considerations, how recent market events have impacted these inputs, and the likely directional impact on the value of a contingent consideration.

|

SHORT-TERM PROJECTIONS OF THE UNDERLYING METRIC (I.E., EBITDA PROJECTION)

|

|

Current Events

|

Companies are assessing how COVID-19 impacts their short-term business prospects and are reevaluating near-term forecasts. As the likelihood of a recession becomes greater and quarantines become more prevalent, many businesses will likely downward revise the near-term forecast of the underlying metric of an earnout.

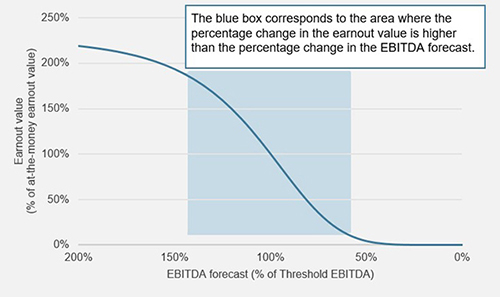

The below figure depicts the change in value of a three-year contingent consideration that pays $1 in each year where the annual EBITDA exceeds a threshold of $100.

Figure 2: Change in Value Due to Changing EBITDA Forecast

(σ = 25%, r = 0.4%, EBITDA/Threshold = 1)

|

|

Value Impact

|

Lowering the forecast of a contingent consideration’s underlying metric (i.e., EBITDA) will most commonly result in a decrease in earnout value.

Depending on the facts and circumstances, the percentage change in the earnout value can be larger than the percentage change in the forecast, due to the nonlinear or option-like relationship between the underlying metric and the contingent payout. Figure 1 highlights the region where the change in contingent consideration value exceeds the change in the forecast.

|

|

COST OF CAPITAL

|

|

Current Events

|

Cost of capital is rising via increasing market risk premiums and costs of debt.

|

|

Value Impact

|

As costs of capital increase, the present value or risk-adjusted forecast will tend to decrease, which will typically result in a decrease in the value of the contingent consideration.

Depending on the facts and circumstances, the percentage change in the earnout value can be larger than the percentage change in the present value of the forecast, as was the case with the possible value change due to changing short-term projections.

|

|

VOLATILITY

|

|

Current Events

|

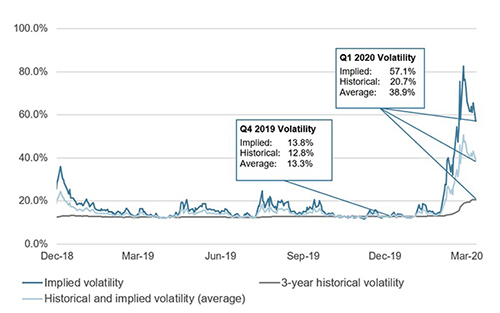

Implied and observed volatility in the financial markets has increased. The Volatility Index (VIX) has increased to 83% in March 2020, as compared to its 14% level in December 2019.

Figure 3: S&P Index Historical and Implied Volatility

Source: S&P Capital IQ; internal research

|

|

Value Impact

|

As market volatility increases, the impact on the earnout value may not be intuitive. Certain structures that are analogous to call options may increase in value, whereas other structures with aggregate caps may decrease in value.

Prior to March 2020, implied and historical volatilities were similar, and a practitioner’s decision to either rely exclusively on historical volatility or blend historical and implied volatilities would not generally be expected to result in significantly different values.

Relying solely on historical volatility measures may not reflect the current market environment, and fair value estimates based on different volatility estimation methodologies may produce divergent values.

|

|

RISK-FREE RATES

|

|

Current Events

|

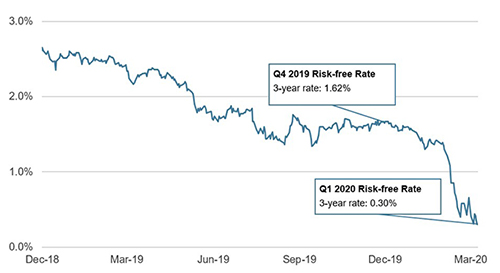

Risk-free rates (typically measured by the U.S. Treasuries) have decreased approximately 130 basis points since December 2019.

Figure 4: U.S. Treasury Yields

Source: S&P Capital IQ; internal research

|

|

Value Impact

|

Decreasing risk-free rates will typically result in a decrease in the value of the contingent consideration.

|

|

CREDIT SPREAD

|

|

Current Events

|

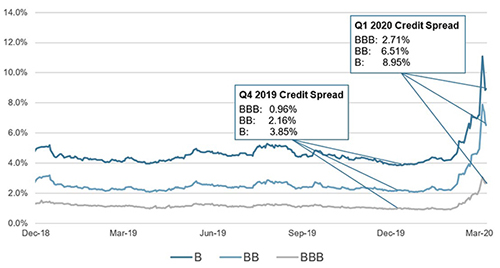

Credit spreads (reflecting counterparty credit risk in the earnout payments) have increased in both investment grade and high-yield credit markets by approximately 175–510 basis points since December 2019, as shown below.

Figure 5: Three-Year Spread-to-Worst of BBB, BB, and B Credit Ratings

Source: S&P Capital IQ; internal research

|

|

Value Impact

|

As credit spreads increase, the value of the contingent consideration will typically decrease.

|

As is the case with any nonlinear or option-like structure, the change in value to a contingent consideration (due to changing certain inputs) is not monotonic. Specifically, the change in certain inputs may have opposite impact on the overall value of the contingent consideration. Companies and valuation specialists should holistically consider the facts and circumstances when assessing the potential change in value to the contingent consideration and the resulting impact on both the balance sheet and income statement.

Other Considerations

For companies contemplating M&A transactions in the current market environment, contingent considerations may provide the following benefits:

- Bridging the valuation gap: In M&A, buyers typically want to avoid paying too much for the acquired businesses and sellers want to avoid selling their businesses for too little. Earnouts allow buyers to pay part of the purchase price only if certain goals are met, while they also allow sellers to receive a higher purchase consideration when the businesses perform to their expectations. With increasing market volatility, contingent considerations can help protect buyers on the downside, while also allowing sellers to potentially receive additional purchase consideration dependent on the future performance of the acquired entity.

- Alternative financing: Depending on the structure of the contingent consideration, it may serve as deferred purchase consideration analogous to seller financing. This deferred nature may provide a lower cost of financing, then current costs of credit.

- Management incentive: Earnouts incentivize sellers to remain involved with, or help contribute to, the future success of the combined businesses in which sellers may be able to receive a higher purchase consideration (when the businesses perform).

Houlihan Lokey has assisted its clients through times of extreme volatility and exogenous events and is ready to assist you today. Please reach out to one of the team members below for more information.

|